Summary

- Despite the decline of the advertising business in Q2, Discovery is still going to be profitable this year and its EPS for FY20 is forecasted to be $2.90.

- By trading at a P/E of 7.64x, Discovery is a great long-term media play with a rich library of content that will continue to create value.

- I’m long Discovery.

Discovery (DISCA) is one of the safest media plays on the market right now. Despite the expected decline of advertising revenues in Q2, the company will still be profitable in the next couple of years. With $1.45 billion in liquidity, the company's debt problem is also manageable as $15.8 billion of its total debt matures in small amounts over the next 29 years. Considering the current low-interest-rate environment, the management of Discovery made a wise choice of approving the $2 billion share repurchase program, which is likely going to be executed in the following months. By trading at a P/E of 7.64x, Discovery is a great long-term media play with a rich library of content that will continue to create value. For that reason, I'm long Discovery.

More Room for Growth

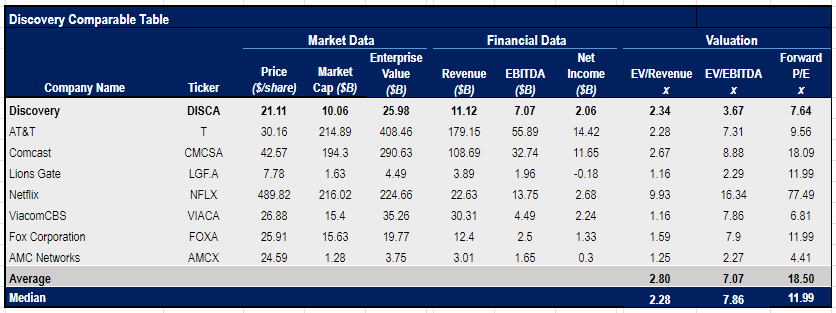

While Discovery's stock declined by more than 30% along with the rest of the market at the beginning of the year, its revenues in Q1 decreased only by 1% Y/Y to $2.68 billion. The company continues to be the most-watched pay-TV network in the United States among all the major demographic groups and COVID-19 only helped it to increase its viewership. When compared to others, Discovery trades way below its peers on an EV/EBITDA and P/E basis and in my opinion, its stock is one of the safest stocks in the media industry to own for the long-term.

Source: Yahoo Finance. The table was created by the author

Since more than 50% of Discovery's revenue comes from the advertising business, the company's Q2 report will show a Y/Y decline of that business, as advertisers currently hoard cash and try to survive the pandemic. Needham estimates that Discovery's revenues in Q2 will be down 14% Y/Y. However, the decline is already priced in and Discovery is not the only company that will be hurt by the pandemic this year. Therefore, Discovery's stock has a high chance to appreciate after the release of Q2 earnings results next week, as there's every reason to believe that the advertising business will recover in the next few quarters.